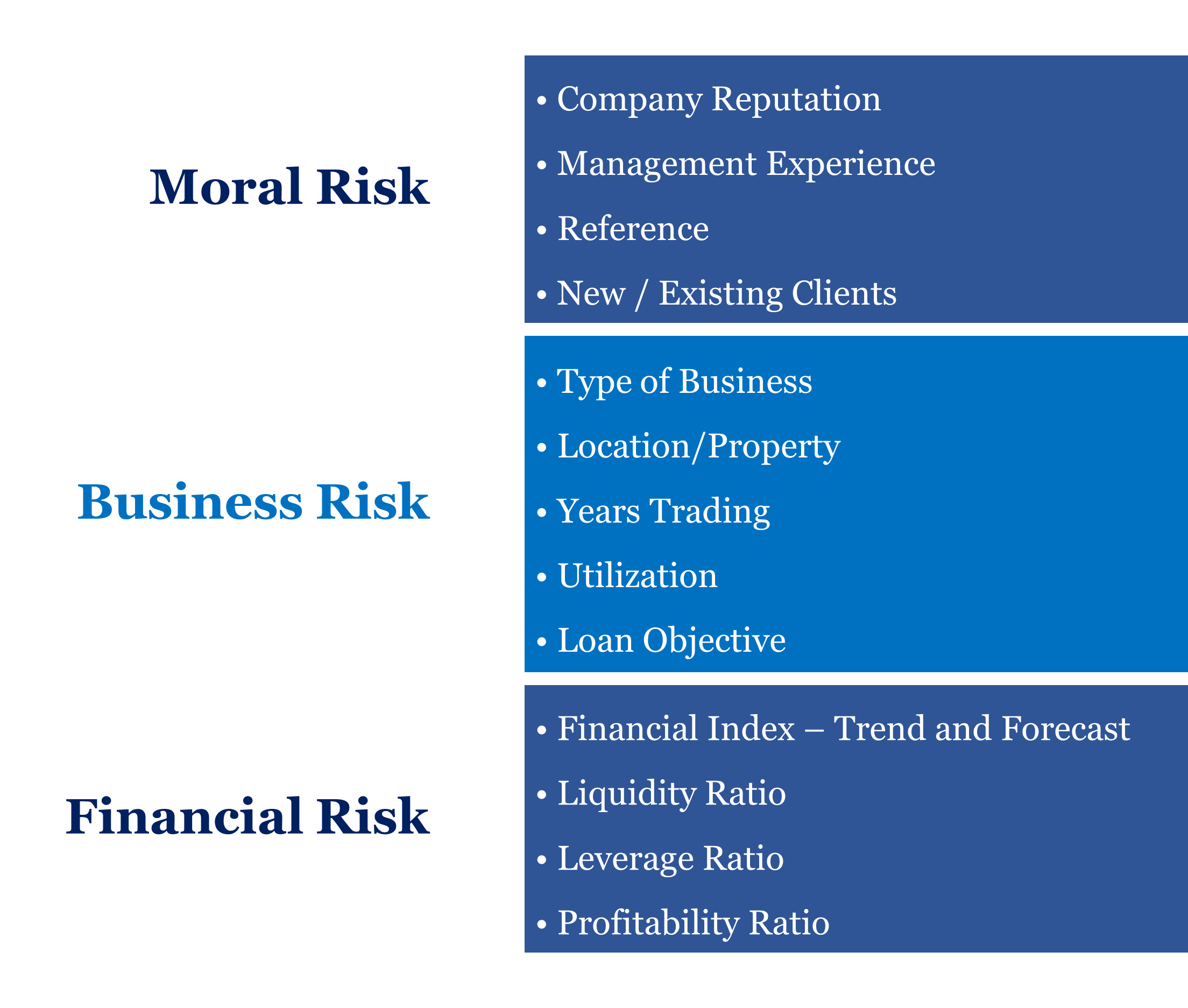

Classical statistical models with robust variable reduction techniques

Champion-Challenger mode of model deployment

Models have a high shelf-life

Well established monitoring & reporting systems

Risk compliance framework well defined

Credit Scoring in the Modern World

Lending to unbanked & under-banked

Limited credit history

Lending apps innovatively collect data on unrelated but indicative aspects

Alternate data is often sparse; is different for each smaller homogenous group

Machine Learning Algorithms perform better in such scenarios

Ensemble of models has shown to improve discrimination power

Limited regulatory oversight

Radix Experience in Credit Scoring

100+ years of collective experience in building credit scoring models

Experience in both, traditional and modern approaches

Clients across multiple domains such as Auto loan providers, SME, Telco, equipment

leasing, insurance providers, e-commerce courier

Experience in building various types of scorecards such as application, behaviour,

collection, fraud, attrition, pre-delinquency scorecards etc.

Case Study

Application Scorecard For SME Bank Loan

Issues & Objectives

To develop application scorecard for SME portfolio of an Indonesian bank

The SME portfolio was new to this bank which had been recently acquired by a

multinational bank headquartered in Australia

The scoring model would be used for SME loan origination decisions

Critical component in the plan for scaling up operations in accordance with Indonesian

government directive

Challenges

The number of data points was very small ≈ 400 making it difficult to obtain reliable

results through predictive modeling

Such sparsity of data is not uncommon in Asia

The SME portfolio was new so the history of defaults had not been well established

Solution & Results

Bootstrapping was used to overcome the limitation of a small sample

Reject rates were taken as a surrogate for default rate

Built high quality scorecard

Process Automation

Ensures Consistency in decision making

Predictive modeling replaces gut feel

Scores re-calibrated with default data after sometime

Case Study

Calibration of Expert Scorecard by ML Methods

Issues & Objectives

For the first time in India, a scorecard was developed for the client to keep vigil on the listed companies to avoid potential financial disaster

Scorecard was based on financial as well nonfinancial events such as changes in auditors, board of directors, litigation, news etc.

The task was to refine expert scorecard with ML methods

Challenges

Listed and unlisted flag was incomplete in the database

Many companies had substantial missing data

Frequent modification of event logic

Running ML models and processing score with new weights took several hours posing a challenge to multiple iteration

Solution & Results

Used modern techniques such as Decision tree, Random forest and Gradient boosting to obtain weights of the events

ML methods were run using h2o

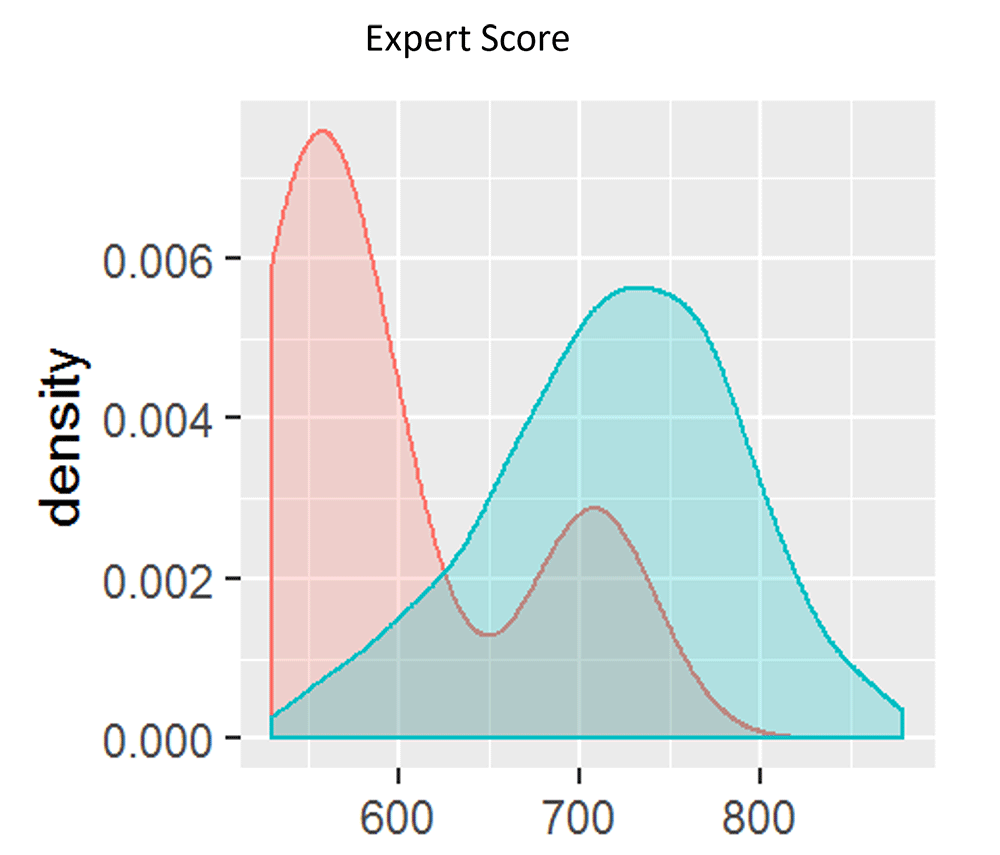

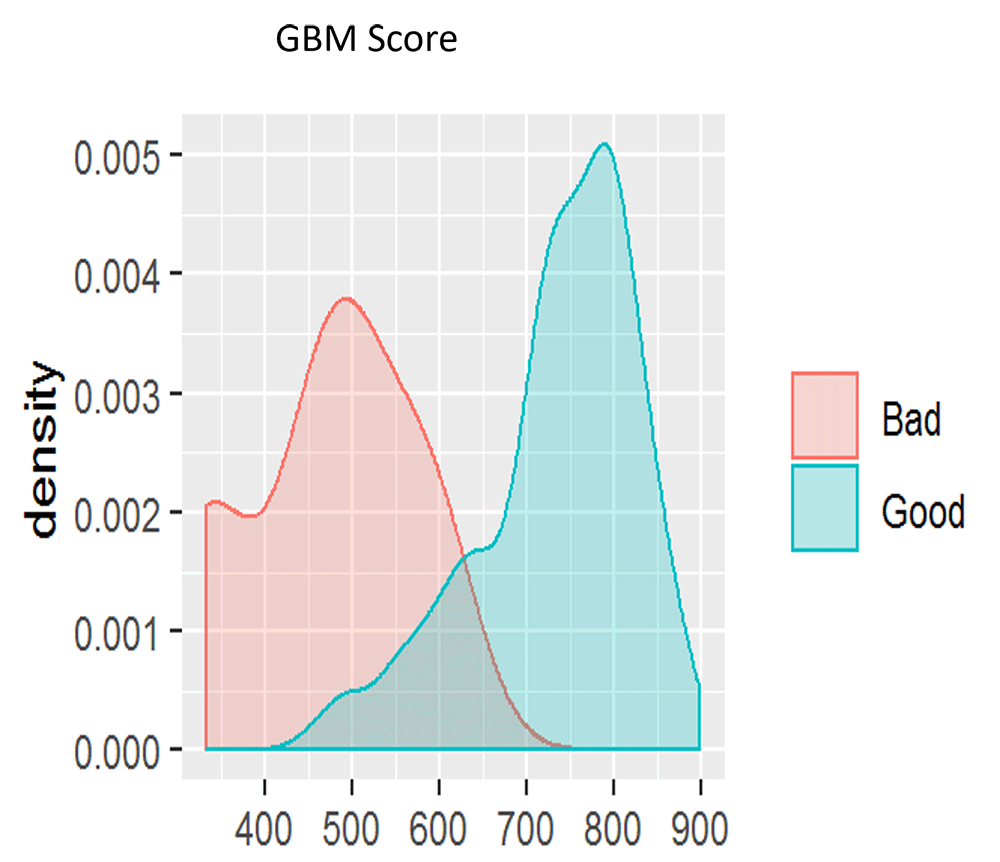

Discriminatory power of the calibrated scorecard was found to be higher than the expert scorecard

Applied a decision overlay which enhanced the predictive power of the scorecard

Better separation between GOOD and BAD companies in modelled score

Expert vs Model Performance

Case Study

Credit Scoring for Leasing Company

Issues & Objectives

A large company in UK finances lease of office equipment, primarily to small and medium companies with ticket size less than £10K

Leased items depreciate rapidly and seizure of collateral does not recover the debt

The company currently cherry picks customers who seldom go bad

They want to expand customer base while controlling risk

For this they want a scorecard to replace rule driven underwriting for better screening

Challenges

Company book identified only 2.5% bad lease – payment history data was fraught with inconsistent figures

After incorporating liquidation/insolvency/dissolution status and rating from credit bureau record, the incidence was boosted to 12%. The process classified non takers of loan into Good and Bad by a logical method and not by reject inference

Many financial fields had substantial missing data

Solution & Results

Scorecards with and without credit bureau ratings were delivered

Discriminatory power of the scorecards were found to be high

4 definitions of defaults were considered

Used various modelling techniques to differentiate between Good, Probable Bad and Definite Bad

Scorecard developed by statistical method replaced purely rule based method

Facilitated work of underwriters by restricting scrutiny to limited proposals

Case Study

Fraud Scoring for Insurance Claims

Issues & Objectives

A major insurance company in Singapore used to manually examine each travel insurance claim to identify potentially fraudulent one

Suspicious claims were subject to a more detailed investigation

This involved considerable manual effort & inconsistent processes

The project objective was to develop a score to identify potentially fraudulent claims which would be subject to greater scrutiny

Challenges

Data included 77,445 claim records of which only 120 had been determined to be potentially fraudulent

So identified potentially fraudulent claims are rare events (0.15%) and therefore hard to detect

It was however expected that there could be a large number of undetected fraudulent claims

Solution & Results

A powerful machine learning algorithm, Gradient Boosting, was used for detecting potentially fraudulent cases

Substantial lift demonstrated. – on the client test data set it sufficed to examine 7.75% of all claims to identify 91.67% of all fraudulent claims

Process automation, ensuring consistency, cost saving and increased accuracy

Scrutiny restricted to high scorers reducing manual work by a factor of 5 -10